What is PAYE?

PAYE stands for ‘Pay As You Earn’. If you’re employed, you may have seen it on your payslip.

It’s the name we’ve given the automatic system we use to collect certain types of tax from people’s wages. Taxes like Income Tax – that’s the tax paid on the money you earn, and National Insurance – the contribution you pay to fund state benefits like the State Pension and the NHS.

Most people pay tax through PAYE

Almost anyone who works for someone else pays their tax and National Insurance automatically through PAYE. If you’re employed full-time, part-time, or in a temporary job, it probably applies to you and probably appears on your payslip.

When you get paid, your employer works out how much you owe, partly by looking at how much you earn in a year. They’ll also work this out using your personal tax code. We’ll explain more about this later.

Your employer then takes what you owe from your wages before they’re paid to you. Then they send this straight to us at HMRC.

If you get money from any workplace or private pensions, your pension provider will also use PAYE.

Key thing to remember:

PAYE means you don’t have any forms to fill in or deadlines to remember. Your employer or pension provider does everything for you.

What tax is paid through PAYE?

Income Tax is the main tax you pay on what you earn. How much you pay depends on which tax rate you are on, which is decided by how much you earn.

You can think of tax rates as like steps on a staircase. As you earn more money, you step up to a higher tax rate. Only the top part of your earnings – the part on that higher step – is taxed at a higher rate, not all of your money.

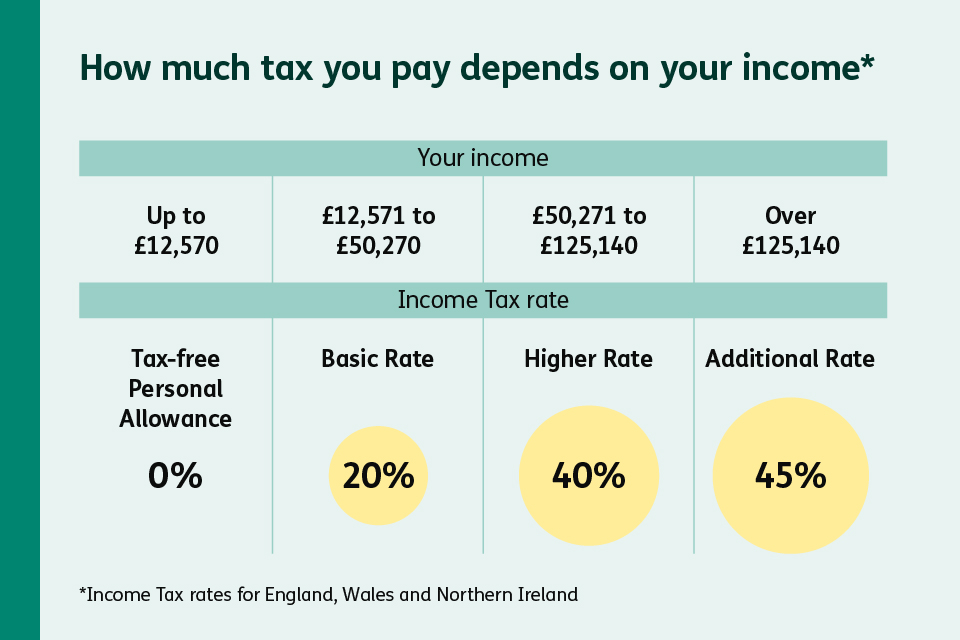

Income Tax rates*

Personal Allowance: Up to £12,570 (0% tax).

Basic rate: 20% on taxable income from £12,571 to £50,270.

Higher rate: 40% on taxable income from £50,271 to £125,140.

Additional rate: 45% on taxable income over £125,140.

*Income Tax rates for England, Wales and Northern Ireland.

The other money paid through PAYE is National Insurance. This goes towards things like the State Pension and the NHS. It’s separate from Income Tax, but it comes out of your pay in the same way. Learn more about it on our National Insurance page.

Both Income Tax and National Insurance appear on your payslip, but on separate lines, so you can see exactly what’s been taken for each.

Everyone on PAYE has a tax code

Your tax code is a combination of numbers and letters which may also appear on your payslip. It’s a code that tells your employer how much money you’re allowed to get in a year before you have to start paying tax.

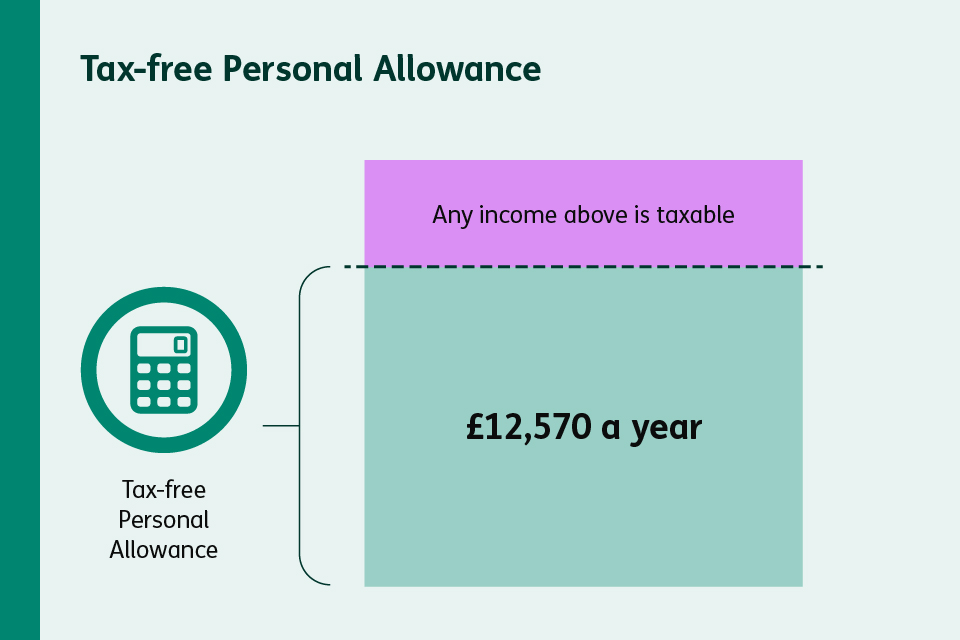

Most people are allowed to get a certain amount of money each year without paying tax on it. This is called your tax-free Personal Allowance. The standard allowance is £12,570 a year. You’ll pay Income Tax on any money above that – this includes any interest or tips, so make sure you let us know about those. The tax code for this allowance is 1257L.

You don’t have to do anything to get a tax code. We work it out when you start a new job and send it to your employer. If your situation changes – like you get a second job or start receiving certain benefits – your tax code might need to change as well. So it’s important that you let us know about any changes.

Helpful tip:

Even though it’s worked out through an accurate, automatic system, it’s good to check your tax code now and then. If it’s wrong, you might pay too much or too little tax. You can check yours quickly and easily on GOV.UK or on the HMRC app.

PAYE also applies to pension income

As we mentioned earlier, because PAYE stands for Pay As You ‘Earn’, it also automatically collects Income Tax from other ‘earnings’ or income – like money you receive from any workplace or private pensions.

Key thing to remember:

The State Pension is different. You’ll always be paid it without any tax taken off – but it does count as taxable income. If your total income, including your State Pension, is more than the Personal Allowance we mentioned earlier, you’ll owe tax.

If you do owe tax, we’ll first try to take it through PAYE on your wages (if you’re still employed), or through any other pensions you have.

You can find out more about how it all works on our Approaching Retirement page.

Not everyone uses PAYE

If you don’t have an employer, you’ll probably have to pay tax in other ways.

If you’re self-employed, you may need to fill out a tax return each year and pay your tax bill directly. This is because you don’t have an employer to handle it for you.

You might also need to do a tax return if you get income from other places, on top of your wages. Like if you get more than £2,500 from renting out a property, or more than £1,000 from self-employment on the side.

PAYE makes paying tax simpler

The aim of PAYE is to make tax easier. You pay what you owe as you go, spread across the year, without having to do anything. No complicated sums and no forms to fill in. We work together with your employer to do it all for you – though you’ll still need to make sure you’re checking your tax code is right and letting us know of any changes.

If you ever think something’s not quite right with your tax, you can check your records online by setting up a personal tax account on GOV.UK or on the HMRC app on GOV.UK. Remember, we’re always here to help.