How the State Pension works

Reaching State Pension age is a big moment.

If you have enough qualifying years on your National Insurance record, you should start receiving some State Pension.

We’ll explain what this means, when payments begin, how much you could get, how to claim, and how tax works in retirement.

Let’s get into it.

When do you start getting paid?

The State Pension age is currently 66, but this will gradually increase to 67 starting in April 2026.

You can easily check your State Pension age using our free calculator on GOV.UK – or on the HMRC app.

How much will you get?

For 2025 to 2026, the full rate of the new State Pension is £230.25 a week – that’s £11,973 a year. The State Pension usually goes up a bit each April, when the new tax year starts.

If you reached State Pension age before 6 April 2016, you’re on the older system called the basic State Pension, where the full rate is £176.45 a week.

Key thing to remember:

Not everyone gets the full rate of the new State Pension. The actual amount you get is based on when you reach State Pension age. To find out how much State Pension you could get, you can check your State Pension forecast on GOV.UK.

You’ll normally need 10 qualifying years on your National Insurance record to receive some of the new State Pension.

If you have gaps in your National Insurance record, you may be able to fill them with what we call ‘National Insurance credits’. Find out all you need to know on GOV.UK.

Helpful tip:

If you can’t fill them with credits, you may be able to fill any gaps that fall in the past 6 complete tax years by paying something called ‘voluntary contributions’.

You can check your National Insurance record on GOV.UK and find out more about how National Insurance works on this page.

How to claim your State Pension

You won’t start getting your State Pension just like that.

About 4 months before you reach State Pension age, you should get a letter from the Department for Work and Pensions showing you how to claim it. You can also find out how to claim it on GOV.UK.

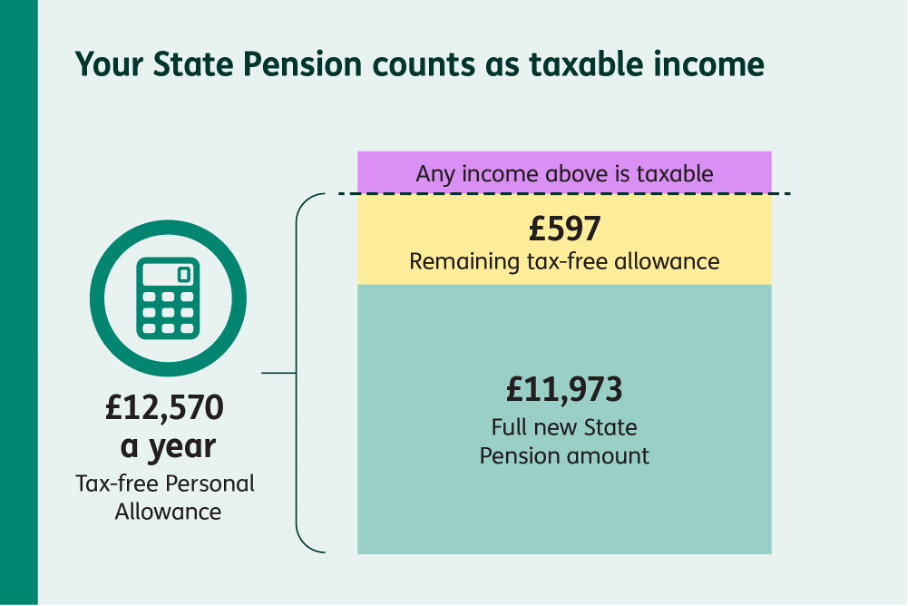

Your State Pension counts towards tax

You might not be aware, but when it comes to working out if you owe any Income Tax, the State Pension is taxable. This means that it counts as part of your income.

Most people are allowed a certain amount of income they don’t pay any tax on. This is called your tax-free Personal Allowance. The current standard Personal Allowance is £12,570 a year. The full new State Pension of £11,973 a year sits just below this. So, if it’s the only income you get, you won’t pay any tax.

However, if you have other income – like workplace or private pensions, interest you get from savings, or part-time work – the full total may push you over your Personal Allowance. You’ll only pay tax on the bit of income that’s above that amount.

Key thing to remember:

You’ll always be paid your State Pension without any tax taken off. But it’s added to any other income you have and counts towards your Personal Allowance.

How tax gets collected in retirement

As you just read, you’ll be paid the State Pension without tax taken off. That means we need to collect any tax you owe later.

If you’re employed and claiming the State Pension, we’ll try to automatically take any tax you owe through ‘Pay As You Earn’ (PAYE). This means you don’t need to do anything.

If you’re retired and receive any workplace or private pensions, we’ll usually collect tax through that. Again, this will happen automatically. We’ll change your tax code to include your State Pension, so your pension provider takes off the right amount of tax.

If you don’t have another pension or work income, and you owe tax on your State Pension, we may send you a Simple Assessment letter. This just shows you how much tax you owe and how to pay. This process is normal and nothing to worry about.

You can find out more about it in our Simple Assessment page.

If you get money in other ways – like from a rented property or self-employment – you may need to fill out a Self Assessment tax return instead.

What about National Insurance?

Once you reach State Pension age, you’ll stop paying National Insurance – even if you keep working. So more of your money stays in your pocket.

Key things to remember:

- you might not get the full rate of the new State Pension. But you may be able to fill any gaps in your National Insurance record to get more. It’s worth finding out where you stand

- you’ll be paid your State Pension without any tax taken off. It counts towards your Personal Allowance, so you may need to pay tax on it if your income goes above your allowance

- if you owe Income Tax, there are a few different ways we’ll try to collect it

You can find out more about it on our National Insurance page.