The most common types of tax

We know that tax can feel confusing, especially because there are different types, each with their own rules. But don’t worry, most people only ever deal with a few, so you don’t need to know everything. Some types may affect you now, others you might come across in the future.

The information in this page will help you understand the 6 main taxes and contributions you’ll come across with us. So that when you do, you know what’s what.

We’ll look at: Income Tax, National Insurance, Value Added Tax (VAT), Capital Gains Tax, Inheritance Tax, and Stamp Duty Land Tax. Each one works differently and applies in different situations.

Income Tax: on money you make

If you make money through working or receiving a pension, you probably already pay the most common type of tax – Income Tax. In most cases your employer automatically takes it from your wages before you get paid. This system is called ‘Pay As You Earn’ (or PAYE), and you can read more about how it works in our PAYE page. In other cases, you may pay through either Simple Assessment or Self Assessment.

People also pay Income Tax on other income they get, like money from pensions, renting out property, or interest from savings. The amount you pay depends on the total amount you make from these things.

Key thing to remember:

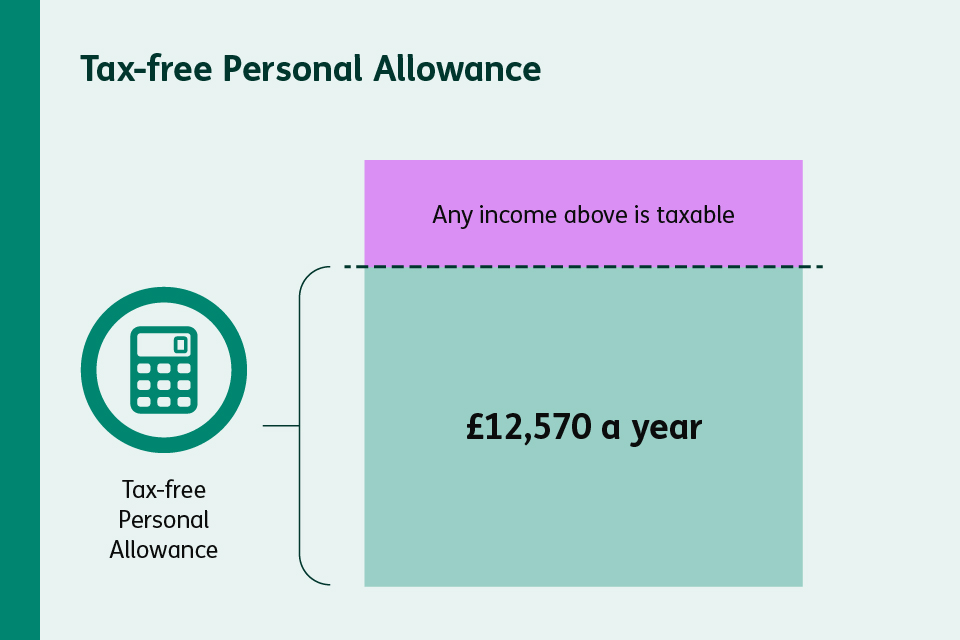

Most people are allowed to get a certain amount of income each year without paying tax on it. This is called your tax-free Personal Allowance. The current standard tax-free Personal Allowance is £12,570 a year.

If your total income is below this amount, you won’t pay any Income Tax. If your total income is higher than your Personal Allowance, you’ll only pay tax on the amount of money above it.

If you’re self-employed or have other income outside of your work, such as interest from any savings, you may need to fill out a tax return. This helps us make sure you pay the right amount of Income Tax and National Insurance (which we’ll get to later).

Depending on your situation, you’ll either fill out a tax return once a year, or send us simple quarterly updates and your yearly tax return through your Making Tax Digital software.

You can find out more about tax returns on our Self Assessment page and Making Tax Digital for Income Tax page.

National Insurance: pays for state benefits

You may have seen National Insurance on your payslip or as part of your tax return and wondered what it is.

You pay National Insurance to help fund things called state benefits – like the State Pension, the NHS, and extra support for more vulnerable people who need it. You pay it in what’s called ‘contributions’.

If you’re employed, your National Insurance contributions will usually be collected automatically through the PAYE system we talked about, just like Income Tax.

If you’re self-employed, you need to do a tax return to see if you owe any Income Tax, like we mentioned in the section above. This also shows us if you owe any National Insurance.

Helpful tip:

Once you reach State Pension age, you stop paying National Insurance. It’s easy to check your State Pension age on GOV.UK. If you’re still working when you reach that point, make sure to show your employer proof of your age, so they can stop taking it from your wages. Don’t worry, if you overpay, we’ll make sure you’re refunded.

VAT: on things you buy

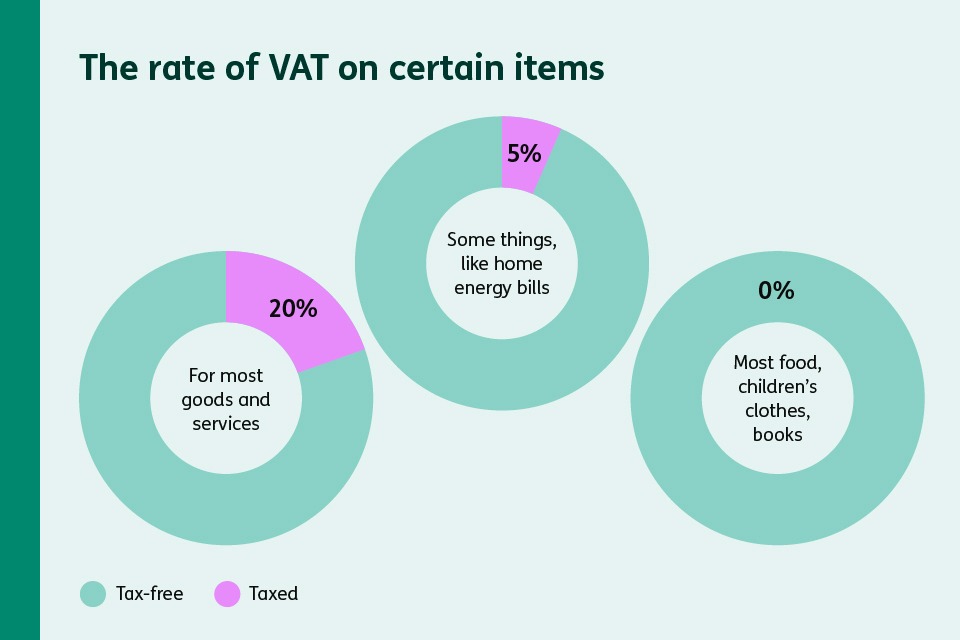

VAT stands for Value Added Tax. When you pay for something – like a haircut, for example, VAT’s automatically included as part of the price.

For most goods and services, VAT is 20%. But some things, like home energy bills, have a lower rate of 5%. Some others, like most food from shops, children’s clothes, and books, have no VAT at all.

You don’t need to do anything to pay VAT. The shop or business collects it and passes it on to us.

Inheritance Tax: on gifts you pass on

When you die, any money, property and belongings you own all make up your ‘estate’. If your total estate is worth more than £325,000, you may need to pay Inheritance Tax. This needs to be paid before your estate can be passed on to your loved ones.

If you leave your estate to your spouse (that’s your married partner) or civil partner, there’s usually no Inheritance Tax to pay at all. And there’s an extra tax-free allowance if you leave your family home to your children or grandchildren. You can read more about how the allowances work on our Inheritance Tax page.

But don’t worry, if you’re receiving an inheritance, you won’t have to work any of it out, that’s up to the people managing the estate.

Stamp Duty Land Tax: on property

When you buy a home or piece of land in England or Northern Ireland, you may need to pay Stamp Duty Land Tax.

Scotland and Wales have their own versions with different names and rates. You can find out how things work in Wales on GOV.WALES and how things work in Scotland on GOV.SCOT.

How much you pay depends on what the property costs. First-time buyers often pay less or nothing at all. However, anyone buying a second property, like a holiday home or a property they rent out, will usually pay a higher rate.

Your solicitor or conveyancer will usually let you know how much Stamp Duty Land Tax is due and when, as part of the buying process. You can find out more and use a Stamp Duty Land Tax calculator on GOV.UK.

Capital Gains Tax: on things you sell

If you sell something for more than you paid for it, you’ve made a ‘profit’ or ‘gain’. Capital Gains Tax is a tax on that gain. For example, if you sell some shares, a second property, or valuable items like art or jewellery from time to time that you no longer want. You don’t pay Capital Gains Tax on everything, generally like your main home, car, or personal belongings worth less than £6,000.

Key thing to remember:

If you’ve got a side hustle and are making or buying things to then sell them for a profit, the money you make is seen as income. So, you’ll pay Income Tax on that money, not Capital Gains Tax.

Just like with Income Tax, most people get a tax-free allowance each year, so you only pay Capital Gains Tax on any profit above that amount. You can read more about Capital Gains Tax in our Selling Assets page.

Helpful tip:

Most people never need to think about Capital Gains Tax. But if you do sell something valuable, it’s worth checking whether you need to let us know.

You don’t need to be an expert

Feeling tax confident isn’t about knowing everything. Even the basics will help you understand what to expect at different stages of life, whether you’re starting your first job, buying a home, or thinking about the future.

Usually, the tax system works quietly in the background. PAYE handles your Income Tax, and VAT is built into prices. For the taxes that do need your attention, like Stamp Duty Land Tax or Capital Gains Tax, there’s always help available.

Remember, if you need to do a tax return, you can get online tools and guidance on GOV.UK.

And if you need to use our Making Tax Digital for Income Tax service, you can find out more on our website.

If you want to explore any of the other taxes we’ve talked about here, you’ll find extra details on our other Tax Confident pages.

Have a look around – because the more you find out, the simpler tax becomes.