Setting up as a sole trader

If you choose to work for yourself – whether you’re a plumber, hairdresser, electrician or freelance designer, then we’re here to help make your tax admin a bit more straightforward.

As a sole trader, you’ll probably need to complete a tax return each year. Here’s how to get started.

A sole trader isn’t a limited company

Being a sole trader means there is no legal difference between you and your business. This is unlike a limited company where you and your personal money are separate from your business.

As a sole trader, you keep all your profits after tax. But you’re personally responsible for your business debts and paying any taxes you owe.

Naming your business

For tax purposes, you can trade under your own name or choose a business name – the choice is yours. So, you can work as ‘Jane Smith’ or create a trading name like ‘Smith Electrical Services’. If you go with a business name, just make sure to include your own name and address on all official paperwork and invoices.

As a sole trader, there’s no need to register your business name with us, though it’s worth checking it’s not already trademarked by someone else.

Registering with us for Self Assessment

If you’re self-employed you may need to complete a tax return. Check whether you need to pay tax and register with us for Self Assessment on GOV.UK.

This is so you can let us know how much money you’ve made and how much you’ve spent running your business (your expenses). We can then make sure you pay the right amount of tax.

Helpful tip:

You’ll only need to register once, but you’ll need to fill out a tax return every year – unless your situation changes.

You can find out more about how to register on our Self Assessment page.

Making Tax Digital for Income Tax

As a sole trader, the way you send us information about your income is changing. It’s called Making Tax Digital for Income Tax. For some people that change starts from April 2026. Making Tax Digital for Income Tax works differently to Self Assessment. You should check if the different rules apply to you.

You can find out who needs to use it, when you might need to start, and how you can get ready for it on our Making Tax Digital for Income Tax page.

How to work out your taxes

When you’re employed, tax comes out of your wages automatically through something called ‘Pay As You Earn’ (or PAYE for short). But when you’re a sole trader, you’ll see how much tax you owe on your tax return.

You’ll include your ‘income’ (money coming into your business) and your ‘expenses’ (money going out of your business). What’s left of your income, once you’ve taken away your expenses, is known as your ‘profit’. You can find out more about what counts as a business expense on GOV.UK.

Depending on how much profit you’ve made, you may need to pay:

Income Tax (this is usually only on any profits over £12,570)

National Insurance

Key thing to remember:

You’ll need to send us your online tax return and pay any tax you owe on or before 31 January, following the end of the tax year. It’s important to do this on time or you could face a penalty.

We cover how to fill out your tax return on our Self Assessment page.

Keeping good records makes tax easier

As a sole trader, you’ll need to keep track of all money coming in and going out of your business. For example, taking a picture of any receipts you’re claiming as a business expense – such as tools or stationery – as soon as you get them is a good idea.

There are plenty of approved free tools online that can help you keep a clear digital record. You can also use accounting software if you prefer. You can find a list of approved software suppliers on GOV.UK.

Key thing to remember:

What matters is that you keep accurate records and can show us what you’ve earned and what you’ve spent on running your business.

Want more tips and advice about keeping track of your business’s money? You can find them on our Record-keeping for small businesses page.

VAT and your business

Value Added Tax (VAT) is a tax that’s added to the things we buy. It’s usually already included in the price. So, as a business, it’s something you’ll need to consider for any products and services you sell.

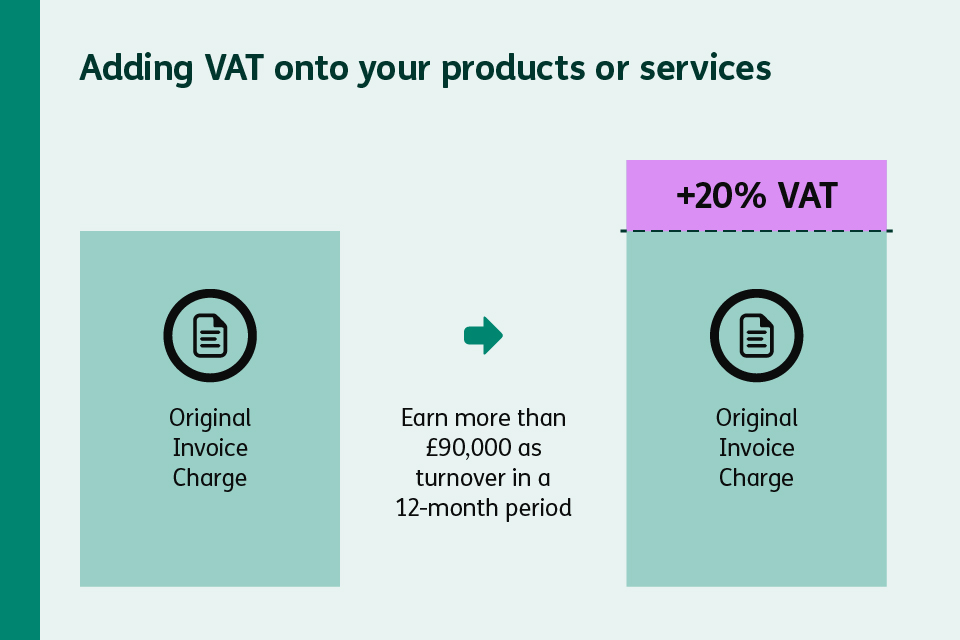

You won’t need to think about VAT until you’ve earned more than £90,000 as ‘turnover’ in a 12-month period. Turnover is the money your business makes before you pay any expenses or tax.

Once you reach this point, you’ll need to register for VAT and make sure you add VAT onto your products or services. This is currently 20% on most goods and services. So if you were charging your customers £100, it would now become £100 + 20% VAT, making it £120.

You can also choose to register for VAT even if you’re not earning over £90,000.

You might choose to do this as it means you’re able to claim the VAT back on some of your business expenses, which can be useful if you’re buying expensive equipment or supplies.

You can find out more on our page for VAT-registered businesses.

Tax info for your industry

Depending on the industry you work in, there may be some extra things you need to know about tax. We cover some of the most common industries for sole traders – including construction, and hair and beauty – on our Tax info for your industry page.

Let’s get you going

You don’t have to figure tax out all on your own – we’re here to help fill in any gaps in your knowledge, so you can get on with doing what you do best.