Working while receiving a pension

Many people choose to carry on working while receiving the State Pension, a private pension, or both. And the good news is that the tax rules are pretty straightforward.

Here’s some handy information to help if you’re planning to work after reaching State Pension age.

Say goodbye to National Insurance payments

If you’re employed, we won’t charge you National Insurance on any money you earn once you reach State Pension age. The State Pension age is currently 66, but will gradually increase to 67 starting in April 2026.

Your employer will stop taking National Insurance from your wages once they have proof of your age. You can show them your passport, birth certificate, or State Pension award letter.

You can also ask us to send them a letter saying you’ve reached State Pension age.

If you’re self-employed, you’ll stop paying all National Insurance contributions from the start of the tax year (6 April) after you reach State Pension age. Remember to put your date of birth on your tax return so we can make sure you stop paying.

Income Tax doesn’t stop in retirement

While National Insurance will stop, Income Tax doesn’t.

You’ll still pay this on your total yearly income. This could come from lots of different places, such as:

- your wages

- if you’re self-employed

- State Pension

- workplace or private pensions

- interest you get from savings

- investments

- rented property

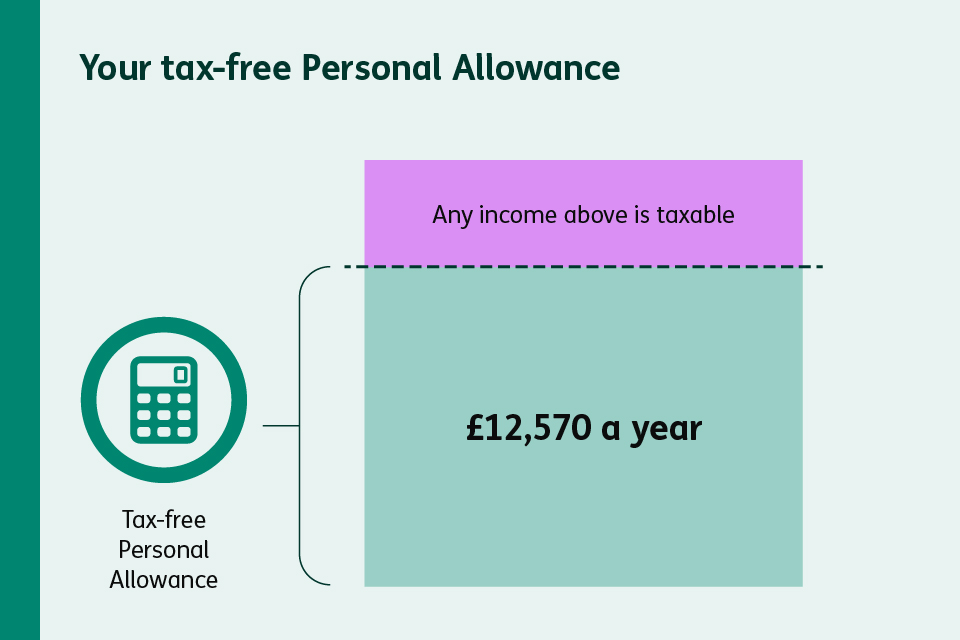

Most people have something called a tax-free Personal Allowance. It’s the amount of money you can get each year before you start paying tax.

The current standard tax-free Personal Allowance is £12,570 a year.

If your total income from work and pensions is below this amount, you won’t pay any Income Tax.

How your State Pension is taxed

1: You’ll always be paid your State Pension without any tax taken off

2: This means it’ll be added to any other income you may have to see if it takes you above your Personal Allowance that year

3: If you do go over your Personal Allowance, then you’ll only pay tax on the amount that’s above it

4: There are a few different ways we’ll try to collect the tax you owe. You can learn about these in the next section

How we collect any tax you owe

If you’re employed, your tax can be collected through ‘Pay As You Earn‘ (PAYE). We give your employer a tax code, so they can work out how much tax they need to take from your wages. You can find out how it works on our PAYE page.

Your tax code is the little set of numbers and letters you may have seen on your payslips. We work it out by looking at your Personal Allowance, plus any other income you may have, including your State Pension.

If you also get a workplace or private pension on top of your wages, we’ll usually change your tax code, so the right amount of tax is taken by your employer and pension provider, and you don’t need to do anything else.

If you’re self-employed, we’ll ask you to list all your income – including any workplace or private pensions – on a tax return. You can then pay any tax you owe straight to us.

You can find out more on our Self Assessment page.

Helpful tip:

If you’re claiming a State Pension and are still working, keep an eye on your payslips to make sure the right amount of tax is being taken.

If something looks wrong – like you think you might have paid too much National Insurance, or you’re not sure if you’re paying the right amount of tax, sorting things out should be simple.

You can easily see what tax you’ve paid on GOV.UK or by using the HMRC app.