Understanding Inheritance Tax

Inheritance Tax is one of those topics that’s easy to put off.

But finding out about it now can give you peace of mind. It can also help you look after your loved ones once you’re no longer around.

What is Inheritance Tax charged on?

Inheritance Tax is charged on the value of your ‘estate’ when you die.

Your estate can include your home, savings, investments, and possessions. It can also include the value of certain items you may have passed on during your lifetime, including any gifts made in the seven years before your death.

Everyone has a tax-free ‘threshold ’ for Inheritance Tax. A threshold is simply a financial limit. This currently means that if your estate is worth less than £325,000, you won’t pay Inheritance Tax on it.

Anything over this £325,000 amount will be taxed at the standard rate of Inheritance Tax, which is 40%.

For example, if your estate is worth £500,000:

- the first £325,000 is tax-free

- the remaining £175,000 is taxed at 40%

- the total tax owed is £70,000

There are other things we call allowances, reliefs and exemptions which may increase your threshold – meaning you can pass on more, tax-free. We’ll talk about these next.

How to increase your tax-free threshold

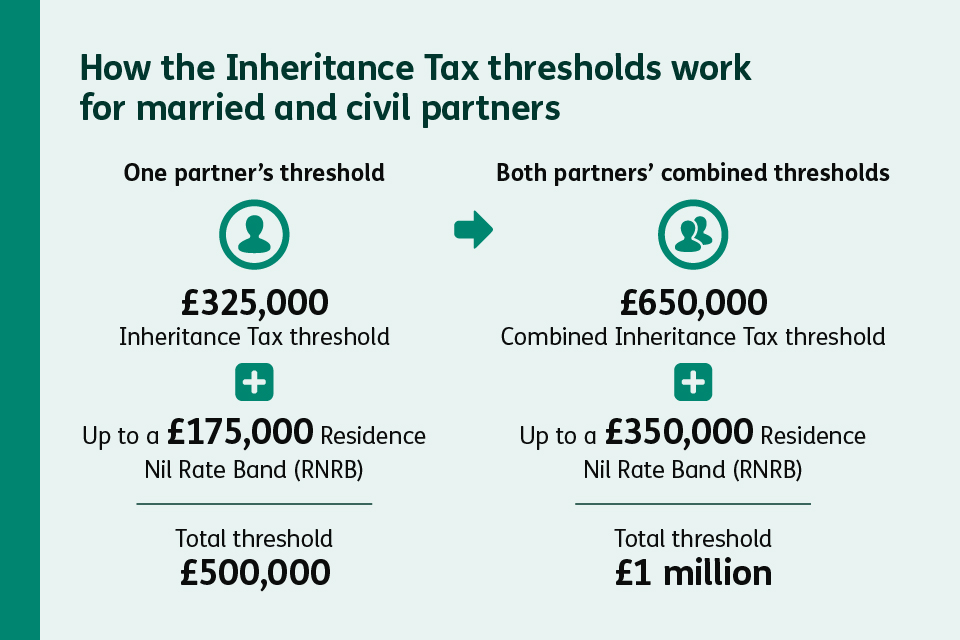

If you leave your home or a share of it to your children or grandchildren, you could qualify for an extra Inheritance Tax allowance called the Residence Nil Rate Band.

It’s worth up to £175,000. Add that to the £325,000 Inheritance Tax threshold we mentioned earlier, and you could pass on a potential sum of £500,000 – without your children or grandchildren having to pay any tax on it.

For married couples and civil partners, this can double to £1 million.

Here’s an example:

You leave everything to your husband, wife or civil partner when you die.

Your £325,000 Inheritance Tax threshold simply transfers over to them. So, when they die, their estate could have a tax-free threshold of up to £650,000 (which is your and their thresholds added together).

This goes up to £1 million if you include the Residence Nil Rate Band allowance.

Key thing to remember:

If your estate is bigger than £2 million, this extra Residence Nil Rate Band allowance goes down by £1 for every £2 over that amount.

You can find out if your estate can benefit from the Residence Nil Rate Band on GOV.UK.

More for married and civil partners

Married and civil partners benefit from something called ‘spouse exemption’. ‘Spouse’ refers to legal partners, ‘exemption’ means it doesn’t apply to you.

It sounds complicated, but it simply means that everything your husband, wife or civil partner leaves to you is totally free from Inheritance Tax, no matter how much it’s worth. You don’t need to apply for it or fill out any special forms – it all happens automatically.

Leaving a tax-free gift while you’re alive

You’re allowed to give away £3,000 worth of gifts each year without them being added to your estate. This means they’re free from Inheritance Tax.

You can give small gifts of up to £250 per person to as many people as you like.

With wedding gifts, you can give £5,000 to a child, £2,500 to a grandchild, or £1,000 to anyone else.

Helpful tip:

Making regular payments from your income, perhaps to help someone with school fees, can also be tax-free – as long as this is money you don’t need and giving it away doesn’t affect your standard of living.

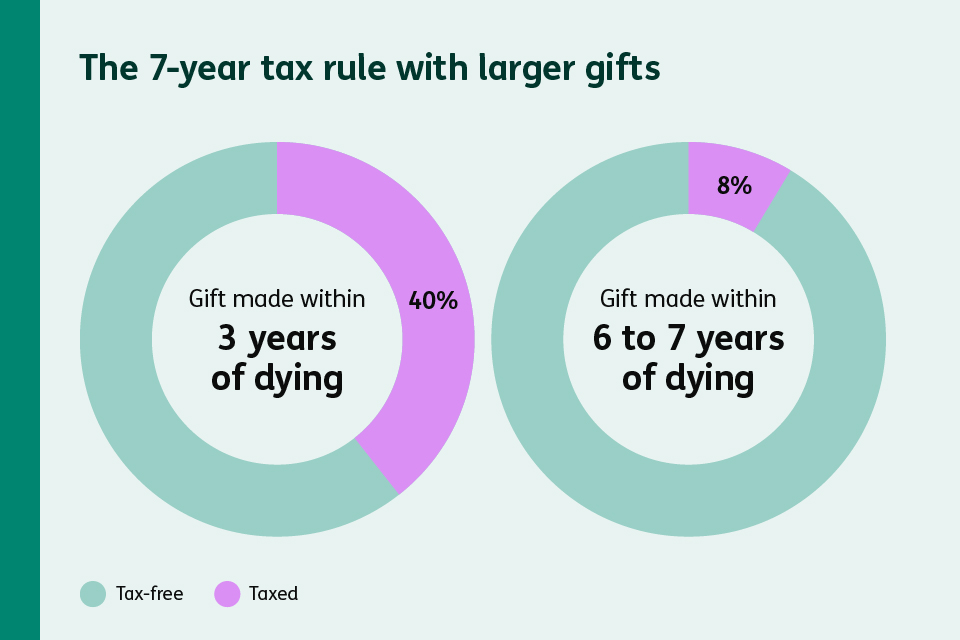

The 7 year rule with larger gifts

If you make a larger gift (more than the amounts we talked about above) and then survive for 7 years or more, it no longer counts towards your estate. This means you won’t pay Inheritance Tax on it.

However, if you die before the 7 years are up, the gift will count towards your £325,000 Inheritance Tax threshold. This will leave less for your estate at the time of your death.

If the gift is more than your available tax-free threshold, the person you gave it to may have to pay tax on it. However, something called ‘taper relief’ can help. This cuts or ‘tapers’ the tax owed, the longer you live after making the gift.

So, for example, if you die within 3 years of making a bigger gift, it’ll be taxed at the full 40%. But if you die 6 to 7 years after making it, it’ll only be taxed at 8%.

Helpful tip:

To help make things easier for your loved ones, remember to keep records of any big gifts you make, including the dates and amounts. It’ll help the person managing your estate to work out what tax is due. You can find out more about gifts and Inheritance Tax on GOV.UK.

What about money left to charity?

Anything you leave to a UK charity is free from Inheritance Tax. And if you pass on at least 10% of your estate to charity, the tax rate on what’s left can drop from 40% to 36%.

Planning ahead gives you options

Getting your head around Inheritance Tax can help you take informed decisions about your estate – and make life simpler for your loved ones.

If the value of your estate is worth less than £325,000, you may not need to do much. If it’s larger or more complicated, understanding what Inheritance Tax you’ll owe on your estate can help you plan.

Writing a will is an important part of this planning. It makes what you want to happen to your estate clear to family and friends. You may also find it very helpful to speak to a financial adviser or solicitor.