Tax when you sell things in retirement

If you’re retired and thinking about selling something like a second home, valuable jewellery or some shares, you might need to pay Capital Gains Tax (CGT).

This is a tax on the profit you make when the item you’re selling has gone up in value. This profit is called your ‘gains’ and the items that you own are called ‘assets’.

You only pay Capital Gains Tax on certain things. And there are allowances that could mean you pay less tax – or even none at all.

Let’s break it down.

We only tax your gains

Capital Gains Tax isn’t charged on the full amount you sell something for. It’s only charged on the gain you make. That’s the difference between what you originally paid and what you sold it for.

In some cases, you can also take off money you’ve spent on the item from your gain. We’ll explain that in more detail later.

Here’s an example:

- you bought shares for £10,000

- you then sell them later for £25,000

- the gain made is £15,000 – so you’ll only be taxed on this amount

Capital Gains Tax doesn’t just come into play when you sell something. It can also be charged if you give something away as a gift, swap it for something else, or get insurance money if an item is lost or destroyed.

Many things you sell are tax-free

You won’t pay Capital Gains Tax on:

- your main home for the time you’ve lived in it

- personal items that you sell for £6,000 or less

- your car

- pensions

- Individual Savings Accounts (ISAs) and most UK government bonds

- gifts to your husband, wife, civil partner or a charity

Things that you might pay Capital Gains Tax on include selling a second home, shares held outside an ISA, valuable antiques, and cryptocurrency.

There are tax-free allowances each year

Just like with Income Tax and the tax-free Personal Allowance, most people are allowed to make a certain amount of gains each year without paying tax on it. This is called your tax-free Annual Exempt Amount.

For 2025 to 2026, your Annual Exempt Amount is £3,000 a year. You’ll only pay Capital Gains Tax on any gains you make above that amount.

If you own things along with your spouse (that’s the name for your legal married partner) or civil partner, you each get your own £3,000 Annual Exempt Amount. This means that together you could make up to £6,000 gains, tax-free.

Key thing to remember:

Your Annual Exempt Amount doesn’t roll over from year to year, so if you don’t use it, you lose it. It refreshes in full at the start of the tax year (every 6 April).

The CGT rate depends on your income

If your income is £50,270 or less, you’ll usually pay Capital Gains Tax at a rate of 18%. If your income more than this, you’ll pay tax on the part that’s at £50,271 or above at a rate of 24%.

That means if the profit you make from selling assets pushes your total income to £50,271 or above, then the part of your gains that’s above this limit (called a threshold) will be taxed at the higher tax rate of 24%. The rest of your gains that are at £50,270 or below will still be taxed at 18%.

Working out whether you owe CGT

You can do that in a few quick steps.

First, work out your gains – that’s the difference between what you originally paid, and what you sold assets for.

Don’t forget to take off any allowable expenses that you may have spent when buying, selling, or improving your assets. For instance, if you’re selling a second home, you could take off the costs of estate agent and solicitor fees. You can also take off the costs of improvement works, such as for an extension. You can’t take off normal maintenance or decorating costs though.

Next, take off your £3,000 Annual Exempt Amount from any gains you made over the year.

If you’ve sold assets for less than you bought them for, you can take off the losses from your gains that year too.

If you’ve got anything left over after you’ve worked everything out, that’s what you’ll pay Capital Gains Tax on.

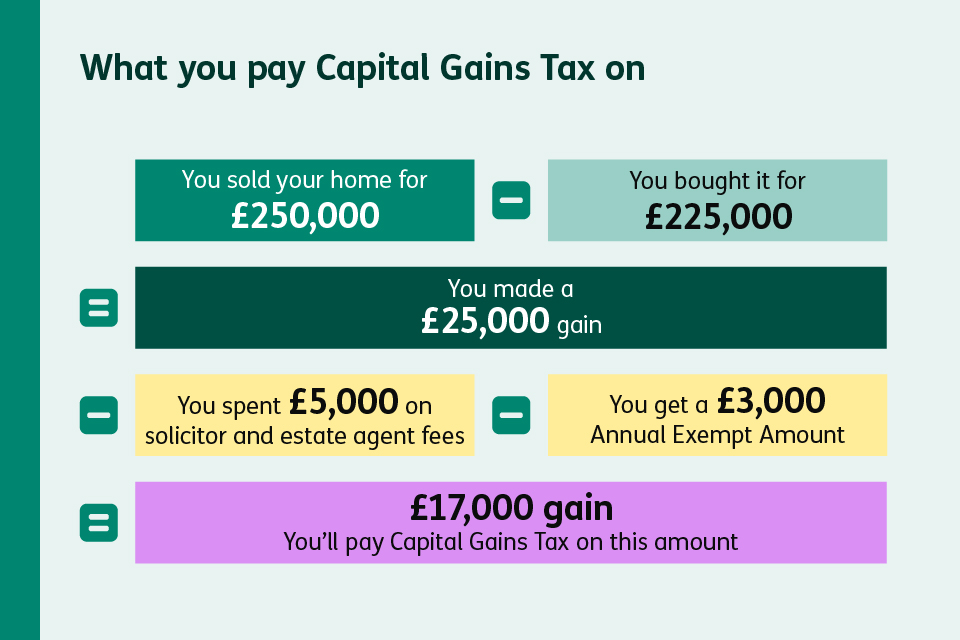

Here’s an example:

Jake bought his second home for £225,000.

He sold it for £250,000. That’s a gain of £25,000.

Jake spent £5,000 on solicitor and estate agent fees.

He takes this away from his gain, then he takes away his £3,000 Annual Exempt Amount.

This leaves Jake with a gain of £17,000, which Capital Gains Tax is due on.

Sold your second home? Let us know

Don’t worry, you won’t usually pay Capital Gains Tax on your home, as long as it’s the only or main place you’ve lived for the time that you’ve owned it.

However, you do pay Capital Gains Tax on second homes if you sell it for more than you bought it for. A second home may be a property you rent out or a holiday home.

Key thing to remember:

If you sell your second home for a profit, you need to let us know and pay the tax you owe within 60 days of completing the sale.

When to tell us you’ve sold assets

Key thing to remember:

If the total amount you sold things for is more than £50,000 (even if your gains are less than £3,000) and you’re registered for Self Assessment, you need to let us know.

However, if your total gains (after your expenses) for the year are below your £3,000 tax-free Annual Exempt Amount, you don’t need to tell us.

Helpful tip:

If you’re thinking about selling something valuable, it’s worth working out if you might have to pay Capital Gains Tax, before you go ahead. You can find more info on how to work this out on GOV.UK.