How losing a partner affects your tax

Dealing with the loss of a partner is incredibly difficult.

The last thing you want to think about is tax. But understanding your situation can help you feel more in control during a tough time.

This page is here to help you.

Your Income Tax and allowances may change

If your spouse (that’s the name for your married legal partner) or civil partner dies, your income may change. You may get money from your partner’s pensions, benefits, or an inheritance. You may need to pay tax on some of this income, and you should let us know about any changes.

You don’t need to let us know about income from your own work or private pensions, ISAs, or if you have a job where tax comes off your pay automatically. This is called ‘Pay As You Earn’ (PAYE) and you can read more about it on our PAYE page.

You also don’t need to let us know if you get the Bereavement Support Payment.

Key thing to remember:

If you or your partner were born before 6 April 1935 and claimed Married Couple’s Allowance, this will stop after the current tax year. The tax year ends on 5 April. Once we know about your change in circumstances, we’ll stop this automatically.

What you can do to take control

When someone dies, you can find a step-by-step guide of what you need to do on GOV.UK.

With our Tell Us Once service, you can let lots of government departments know about your partner’s death in one go. It’s here to save you time and stress, when you’re already having to deal with a lot.

You may be aware there’s emotional support available when you lose a partner, but there can be financial support too.

If you’re not sure about your position, consider chatting to a solicitor or financial adviser. They can help you explore your options and make sure you don’t miss out on any extra support. Many offer free initial consultations.

Were you married or civil partners?

If you were either of these when your partner died, you benefit from something called ‘spouse exemption’. ‘Exemption’ means it doesn’t apply to you.

It sounds complicated but it simply means that everything your spouse or civil partner leaves to you is totally free from Inheritance Tax, no matter how much it’s worth. You don’t need to apply for it or fill out any special forms – it all happens automatically.

There’s something else too.

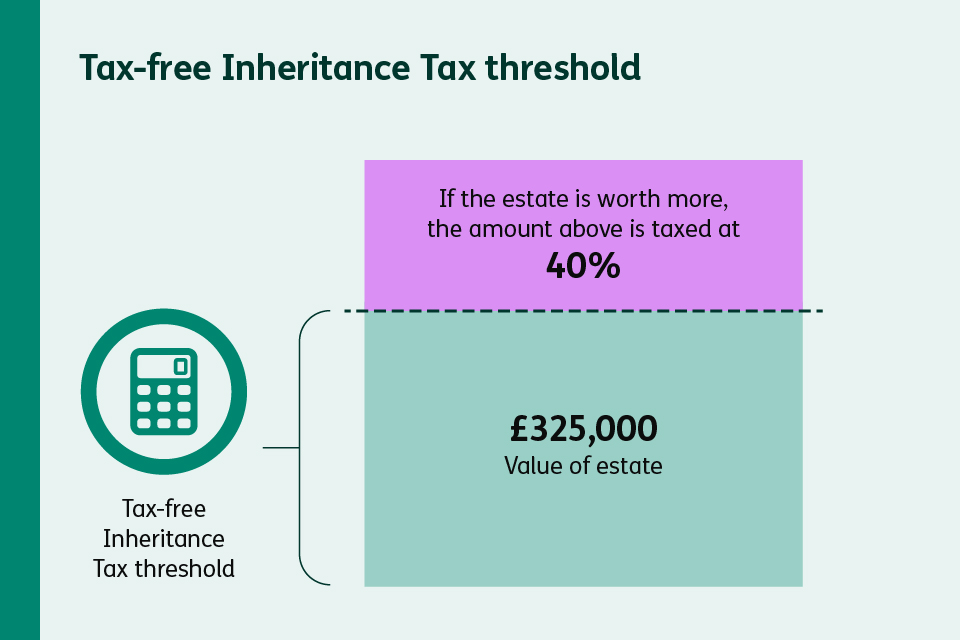

Everyone has a tax-free amount, or ‘threshold’ for Inheritance Tax – this is the amount of money you can inherit before you need to pay tax on it. This currently means that if someone’s estate is worth less than £325,000, no Inheritance Tax is paid on it. ‘Estate’ is the name for everything of value that someone owns.

If your spouse or civil partner didn’t use all of their Inheritance Tax threshold, any unused amount can be transferred to you. So, when you die, your estate could have a total tax-free threshold of up to £650,000.

If your spouse or civil partner has left the family home or a share of it to children or grandchildren, there may be an extra Inheritance Tax allowance called the Residence Nil Rate Band. It’s worth up to £175,000.

This can be transferred to your spouse or civil partner too, and it may increase your Inheritance Tax threshold as a couple to £1 million.

Here’s an example:

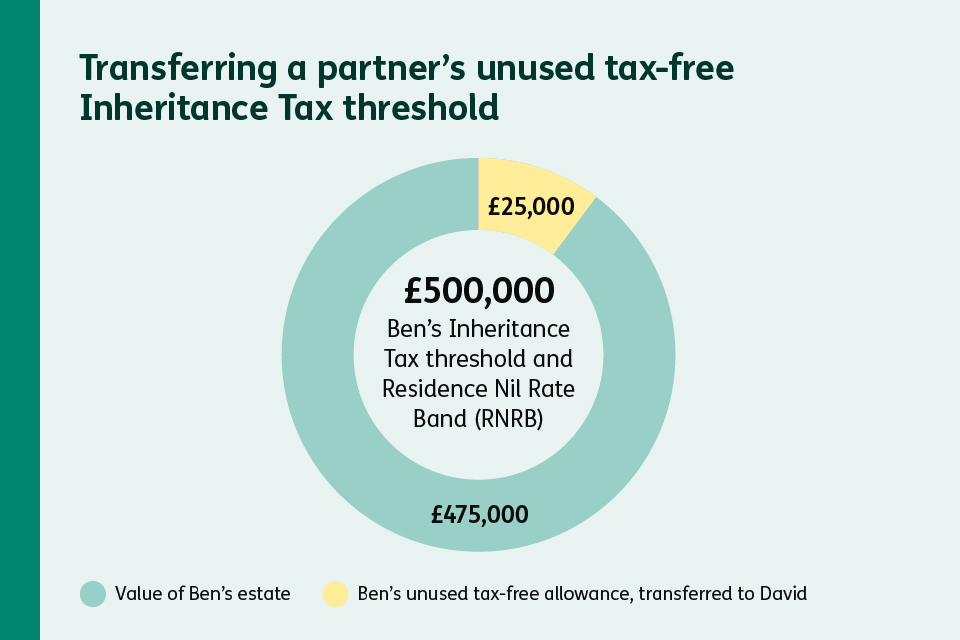

Ben and David were civil partners.

When Ben died, he left his share of their family home to their child, Lucy.

Because of the Residence Nil Rate Band, Ben had a total Inheritance Tax threshold of £500,000.

Ben’s share of the family home was worth £475,000. Because he didn’t use all of his Inheritance Tax threshold, the remaining £25,000 is automatically transferred over to David’s future Inheritance Tax threshold.

This makes David’s future Inheritance Tax threshold worth £350,000. That’s made up of the standard £325,000 threshold, plus the £25,000 Ben transferred to him.

David can also benefit from the Residence Nil Rate Band on top.

You can find out more about how this works on our Inheritance Tax page.

Capital Gains Tax when you inherit

You normally pay Capital Gains Tax if you sell something you owned (like a second home or valuable jewellery) that has gone up in value. This is called making a ‘gain’.

When you inherit an item, if you dispose of it in the future, you’ll only pay tax on the part of the item that’s increased in value since the person died.

This reset of the item’s value is called an ‘uplift’. You’ll get this uplift whether you were married, civil partners, or living together.

Here’s an example:

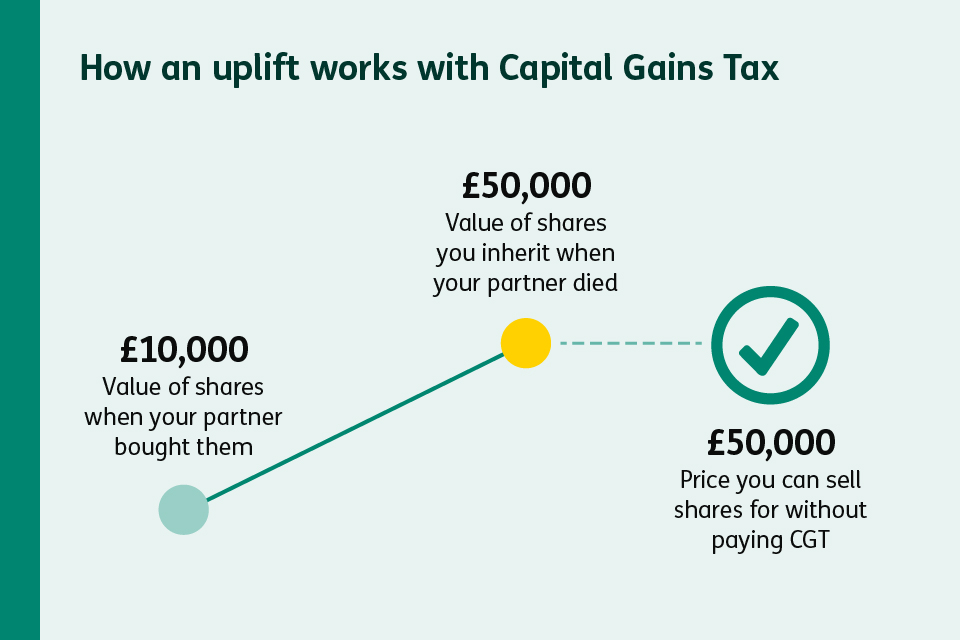

- your partner bought shares for £10,000

- when they died, the shares were worth £50,000 and you inherited them

- if you later sell those shares for more money, you’ll start working out what Capital Gains Tax you owe from the £50,000 value

- you’ll only pay Capital Gains Tax on any gains made above £50,000, not the £10,000 your partner paid for them

You’ll still get your yearly Capital Gains Tax allowance – the amount of profit or gains you can make without paying any tax – as normal. You can find out more about Capital Gains Tax rates and allowances on GOV.UK.

If your gains are higher than your yearly Capital Gains Tax allowance, you can see how to let us know and pay on GOV.UK.

What about if you lived together?

If you lived together, but weren’t married or civil partners, the Inheritance Tax rules are very different. No matter how long you’ve been a couple, your inheritance won’t get ‘spouse exemption’.

So, if everything your partner owned (their estate) and left to you was worth more than the £325,000 Inheritance Tax threshold, you may have to pay Inheritance Tax on any money above this amount.

This includes their share of anything you both owned jointly and you inherit automatically. The standard Inheritance Tax rate is 40%. Your partner’s unused tax-free threshold also can’t be transferred over to you, but you do get your own threshold.

Work through things at your own pace

You don’t need to deal with everything at once. Most tax deadlines give you the time and space to focus on what matters most.

Understanding your position is the first step forward. And when the time’s right, there are people and services always ready to help you at every stage, find more information on GOV.UK.