Approaching retirement

Retirement is a life-changing moment.

One thing you may find different is the way you get and manage your money changes. Instead of getting regular money through working, you might get money from lots of different places – pensions, savings, and maybe other sources too.

The good news is that once you understand how things work, looking after your money can be straightforward.

Tax in retirement works like usual

You’ll simply add up all the money you get each year (your income) from things such as your State Pension, any workplace or private pensions, investments, rented property and self-employment.

You’ll use this to work out if you owe any tax. For some people, a chunk of their income will be tax-free. This is called a Personal Allowance.

The current standard tax-free Personal Allowance is £12,570 a year.

If you get a Personal Allowance and your income goes over that amount, you’ll start to pay tax on it. The rates you pay are separated into ‘thresholds’. A threshold is simply a financial limit.

Income Tax rates

| Your income | Your Income Tax rate |

|---|---|

| Up to £12,570 | 0% (Tax-free Personal Allowance) |

| £12,571 to £50,070 | 20% |

| £50,071 to £125,140 | 40% |

| Over £125,140 | 45% |

If you live in Scotland, the rates are slightly different. You can find the Scottish rates of Income Tax on GOV.SCOT.

Helpful tip:

You’ll only be taxed the higher rate on the amount of money that’s above each threshold, not your total income.

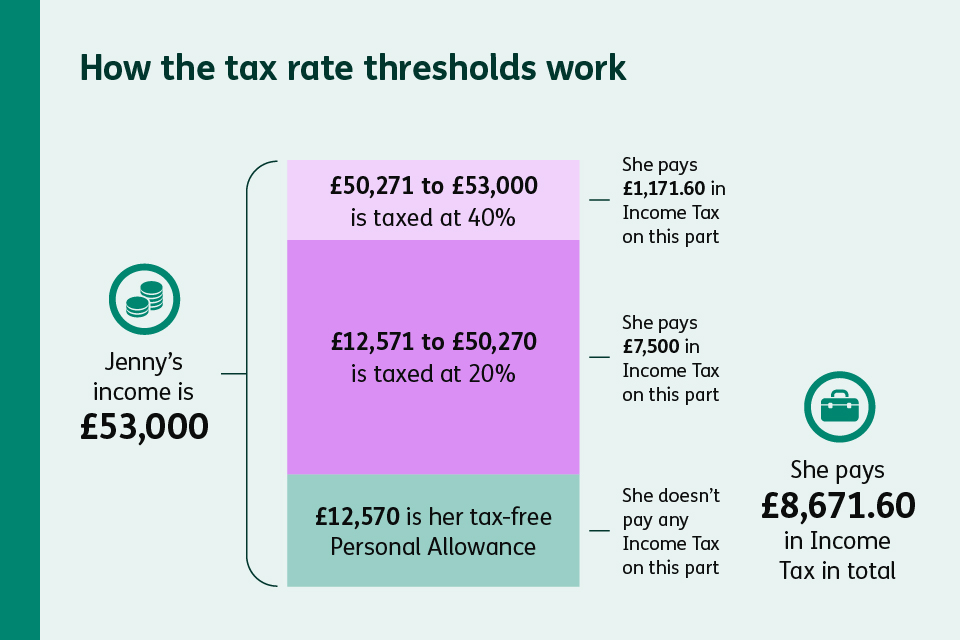

Here’s an example:

Jenny gets £53,000 from her State Pension and a private pension.

£12,570 is her Personal Allowance. This is tax-free.

The bit of her income between £12,571 and £50,070 is taxed at 20%. This means she pays £7,500 in Income Tax on this part.

The bit of her income between £ 50,071 and £53,000 is taxed at 40%. This means she pays £1,171.60 in Income Tax on this part.

So, in total, Jenny pays £8,671.60 in Income Tax.

How the State Pension works

Once you reach State Pension age, you can claim the State Pension. This is a regular payment from the government. The State Pension age is currently 66, but will gradually increase to 67 starting in April 2026. You can easily check your State Pension age on the HMRC app or by using our free calculator on GOV.UK.

For 2025 to 2026, the full rate of the new State Pension is £230.25 a week – that’s £11,973 a year. The State Pension usually goes up a bit each April, when the new tax year starts.

Key thing to remember:

Not everyone gets the full rate of the new State Pension. The actual amount you get is based on when you reach State Pension age. To find out how much State Pension you could get, you can check your State Pension forecast on GOV.UK.

You’ll normally need 10 qualifying years on your National Insurance record to receive some of the new State Pension.

If you have gaps in your National Insurance record, you may be able to fill them with what we call ‘National Insurance credits’. Find out all you need to know on GOV.UK.

Helpful tip:

If you can’t fill them with credits, you may be able to fill any gaps that fall in the past 6 complete tax years by paying something called ‘voluntary contributions’.

How your State Pension is taxed

1: You’ll always be paid your State Pension without any tax taken off

2: This means it’ll be added to any other income you may have to see if it takes you above your Personal Allowance that year

3: If you do go over your Personal Allowance, then you’ll only pay tax on the amount that’s above it

4: We’ll usually try to collect any tax you owe through your wages – if you’re still employed, or through any workplace or private pensions you have. If we can’t collect tax this way, we may send you a Simple Assessment letter instead

5: It all happens automatically. We’ll simply change your tax code to tell your employer or pension provider how much money to take off before you’re paid. Or we’ll send you a letter to let you know what you owe

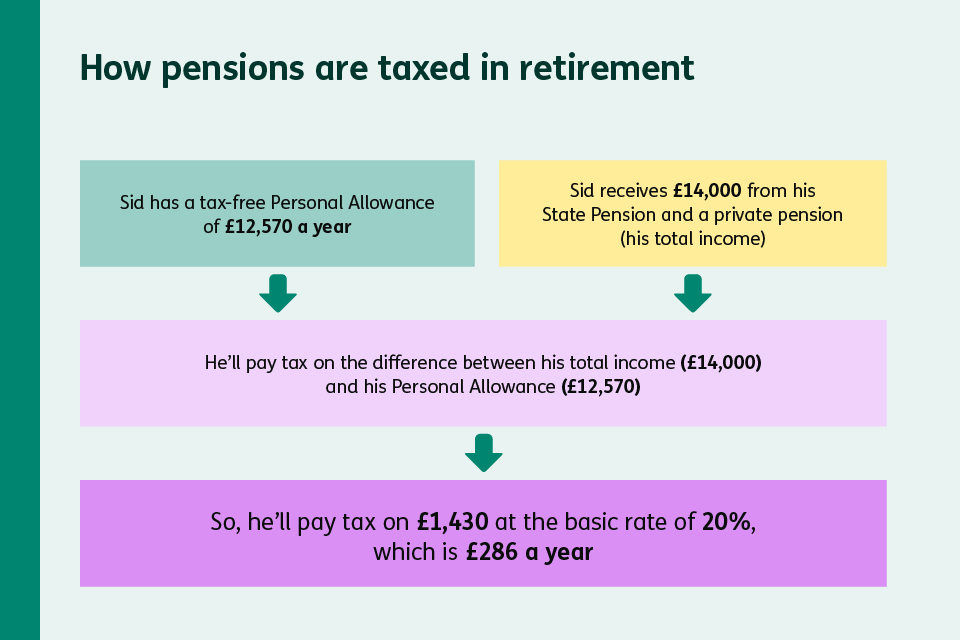

Here’s an example:

Sid has a Personal Allowance of £12,570 a year – that’s all tax-free.

He’s retired and receives £14,000 from his State Pension and a private pension. This is his total income that year.

He’ll pay tax on the difference between his total income (£14,000) and his Personal Allowance (£12,570).

So, he’ll pay tax on £1,430 at the basic rate of 20%, which is £286 a year.

Workplace and private pensions

A lot of people may have workplace or private pensions. There are three main types of pension. These are called Defined Contribution, Defined Benefit and Collective Defined Contribution schemes.

Defined Contribution

These pensions are basically a pot of savings which you and your employer have paid into over the years. When you want to take money out, there are a number of ways to do this. You can:

- choose to be paid a lump sum

- take out regular amounts (you may hear this called ‘draw-down’)

- use part or all of your savings pot to buy something called an ‘annuity’. This acts like a guaranteed salary, so you’ll get fixed and regular payments for an amount of time that you choose

Defined Benefit

These pensions are also called ‘final salary schemes’. With these types, you get a fixed regular income for the rest of your life, rather than your money sitting in a pot. The amount you get is based on both your salary and the number of years you’ve worked.

Collective Defined Contribution

These are a newer type of pension. They’re a bit of a mix of the first two pension types.

Just like a Defined Contribution pension, you and your employer pay into a collective pot. Other people’s money is pooled together with yours. Then, just like with a Defined Benefit pension, you’ll get a regular income for life when you’re ready to take it. However, the amount that you get as an income isn’t guaranteed.

Taking some of your pension tax-free

At the moment, you can begin to receive money from a Defined Contribution pension from the age of 55 (this will rise to 57 from April 2028).

You can usually take up to 25% of your pension pot as a tax-free lump sum – up to a maximum of £268,275 for most people.

You don’t have to take this 25% in one go. You can withdraw small amounts every now and then, leaving the rest invested – and hopefully growing.

Key thing to remember:

When you start taking money from the remaining 75% of your pension pot, it’s seen as taxable income. So, it’s worth remembering that if you take a large chunk in one go, and you have income from other sources on top, you might end up paying a higher rate of tax.

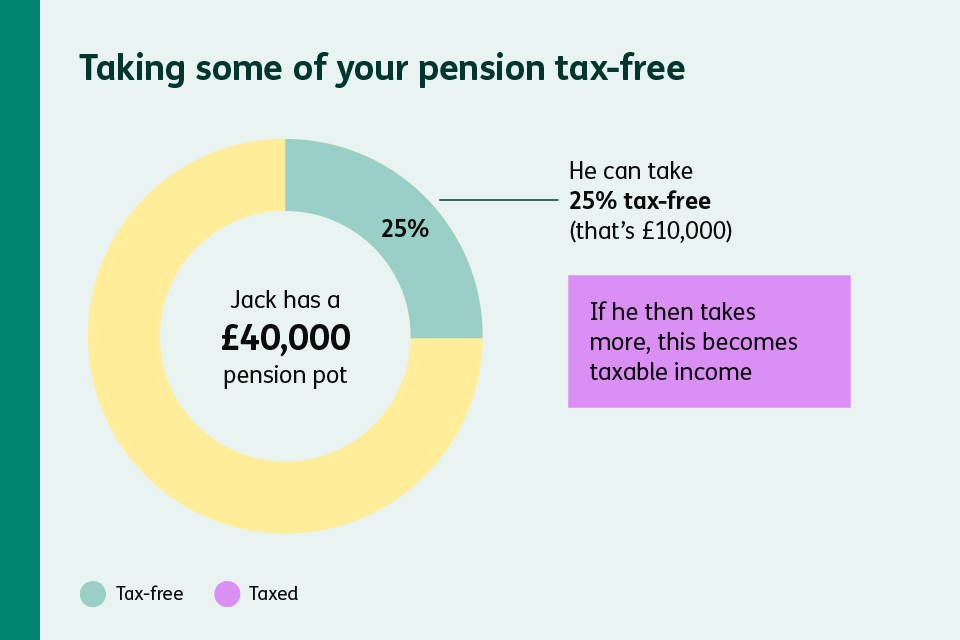

Here’s an example:

Jack has a £40,000 pension pot.

He can take £10,000 tax-free.

If he then takes a further £5,000, this becomes taxable income.

It gets added to any other income he gets to work out if he owes any tax – and how much.

Your tax code and your pensions

Your tax code is the little mix of numbers and letters that show how much tax-free allowance you get.

It might look like this: 1257L, S330L, K150.

The numbers are your tax-free allowance divided by 10, so 1257L means your allowance is £12,570 a year.

The letters are the tax status we give you. L means you get the ‘standard allowance’. BR means you get no allowance and pay tax at what’s called the ‘basic rate’. K means you owe tax, and so on.

You can find out more information about tax codes and how they work on our Understanding your tax code page.

Your tax code is especially important when you retire, because your income may now come from several different places. It tells your pension provider how much tax to take from your pension, before you’re paid it.

If your pension payments suddenly go up or down, it often means your tax code has changed. Your tax code may change if:

- you take a lump sum from your pension

- you take regular money from a pension

- you start taking money from a new pension

- you start receiving the State Pension

- your State Pension increases in the new tax year

- your income changes

- we adjust previous underpayments or overpayments

- you move abroad

Helpful tip:

If your tax code is wrong, you may pay too much or too little tax. It’s worth looking over your tax code and pension payslips regularly to check everything looks right.

Will you still pay National Insurance?

The simple answer is no.

Once you reach State Pension age, we don’t charge you National Insurance anymore – even if you keep working. That means more take-home pay for you.

If you’re still working, simply show your employer proof of your age and they’ll stop taking National Insurance from your pay. However, you’ll still pay Income Tax.

Pension Credit can top up low income

If you’re over the State Pension age and on a lower income, Pension Credit can help. For example, Guarantee Credit tops up your weekly income to at least £227.10 if you’re single, or £346.60 for couples.

Helpful tip:

Pension Credit also unlocks other support, like help with housing costs and Council Tax, free NHS dental treatment, and a free TV licence if you’re 75 or over.

You can claim even if you own your home or have savings. Have more than £10,000 in savings? This will affect how much help you get, but you can still make a claim. Find out how to claim Pension Credit on GOV.UK.

3 ways we collect tax in retirement

1. Pay As You Earn (PAYE)

We’ll usually use this system to take any tax you owe from your workplace or personal pensions. Your pension provider will take off tax, before you’re paid. This will be the case for most retired people.

Key thing to remember:

Your State Pension is different – you’re paid this without any tax taken off. That means we’ll try to take any tax you owe on your State Pension by taking it off your other pensions instead.

2. Self Assessment

You’ll need to do a Self Assessment tax return if you have other income that we can’t tax automatically. This could be money you get from:

- renting out a property

- self-employment

- high interest from savings or investments

If you haven’t done a Self Assessment before, don’t worry. You’ll soon get the hang of it. Our Self Assessment page can help you get started.

3. Simple Assessment

We use Simple Assessment in retirement when we need to collect tax from you, but you don’t have a pension or job that means we can collect it automatically.

We use this for people with straightforward tax situations, who don’t need to do a full Self Assessment. We’ll simply send you a letter that lets you know:

- your income

- any tax you owe

- how to pay it

Key thing to remember:

We know that getting a letter from us may seem scary. But don’t worry, it’s a totally normal process and you haven’t done anything wrong. You can find out more about how it works on our Simple Assessment page.

How to work out your retirement income

Start by checking how much of the new State Pension you’ll get. As we mentioned earlier, your National Insurance record matters here. It’s quick and easy to check yours on the HMRC app or with our free calculator on GOV.UK. You can also see if you can fill any gaps to help boost your new State Pension.

Next, find out about any workplace or private pensions you have. Your pension providers can give you statements showing you how much money you’re likely to get.

There’s lots of extra help out there too. MoneyHelper’s free pension calculator can show you how everything fits together. And, if you’re over 50 and have a Defined Contribution pension, you can get free guidance from the government’s Pension Wise service.

Understanding where your money will come from when you’ve retired is a good move. It’ll help you manage your money and make confident decisions about your future.