Tax in the construction industry

When it comes to tax, there are a few things you need to know if you work in the construction industry. We’re here to help you understand the basics so that you can stay on top of your tax and avoid any common mistakes.

The difference between contractors and subcontractors

You probably already know this, but a customer will hire a contractor to manage a construction project. The contractor will then hire subcontractors who are skilled in specific trades to help with the project. This is important as there are some key differences between how contractors and subcontractors pay tax.

How the Construction Industry Scheme works

The Construction Industry Scheme applies to most construction work in the UK. It covers jobs like building, repairs, decorating, demolition and installing heating or plumbing systems.

Under the Construction Industry Scheme, if you work as a subcontractor, the contractor will usually take some money from your pay. This money goes straight to us and works as an advance payment towards your yearly Income Tax and National Insurance bill.

All contractors have to register for the Construction Industry Scheme but, as a subcontractor, you can choose to or not.

Helpful tip:

If you do register, then you’ll have less money taken, or ‘deducted’, from your pay. This doesn’t mean that you pay less tax overall. But it does mean that you have more cash flow throughout the year, and you’re less likely to have overpaid tax so you won’t need to apply for a refund.

You can register for the Construction Industry Scheme for free on GOV.UK.

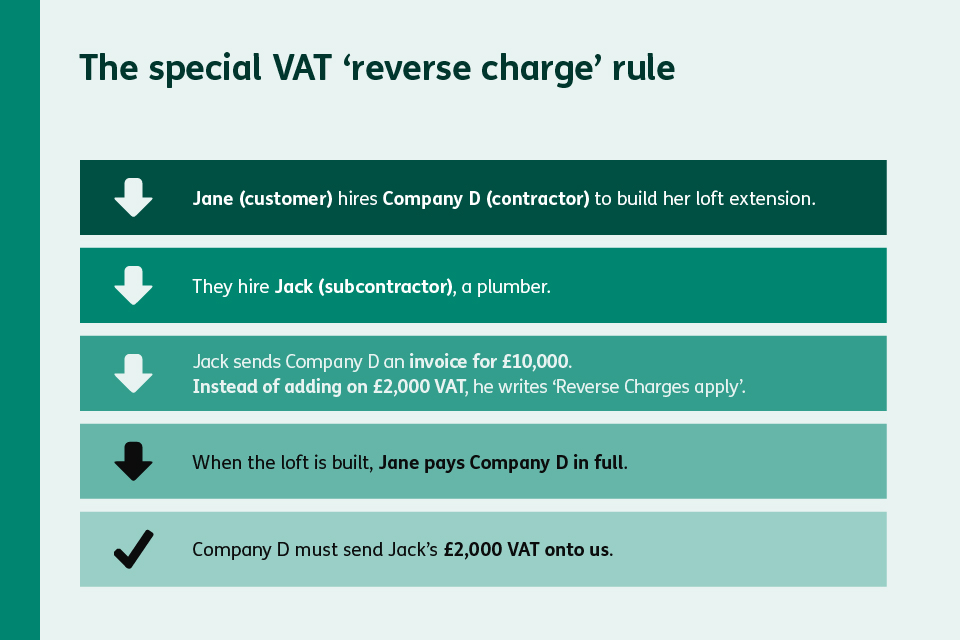

A special VAT rule: the ‘reverse charge’

If you’re VAT-registered, construction has a special rule called the ‘reverse charge’. This helps to combat fraud and applies when you do building work for another VAT-registered business, that will pass that work on to their own customer.

Key thing to remember:

With the reverse charge, you don’t add VAT onto your invoice. Instead, your customer (the VAT-registered contractor who hired you) handles the VAT themselves. Your invoice should clearly show that the reverse charge applies, and the amount of VAT you would have charged – and that your contractor now owes.

Here’s an example:

Jane hires Company D to build her loft extension.

Company D are the contractor.

They hire Jack, a plumber, as a subcontractor.

After his work is done, Jack sends Company D an invoice for £10,000. Instead of adding on the £2,000 VAT, he writes ‘Reverse charges apply. Customer to pay £2,000 VAT to HMRC’.

When the loft is built and Jane has paid Company D in full, Company D must send Jack’s £2,000 VAT onto us.

The reverse charge doesn’t apply when you work directly for the end customer. For example, Company D can’t ‘reverse charge’ Jane. They must charge her VAT on their invoice.

You can find out more about the reverse charge for VAT on GOV.UK.

Are you employed or self-employed?

When it comes to tax in construction, it’s important to know if you’re either employed or self-employed. This is called your ‘employment status’. It’s decided by how you actually work day-to-day, not just what your contract says.

Being registered with the Construction Industry Scheme doesn’t automatically mean you’re self-employed.

Knowing your employment status

You’re probably employed if:

- someone else books jobs for you

- someone else sets your working hours

- someone else provides your tools and equipment

- you can’t send someone else to do the work in your place

You’re probably self-employed if:

- you decide when and where you work

- you find your own jobs and set your own prices

- you buy your own products and equipment

- you only earn money when you have bookings

- you invoice clients for the work you do yourself

Key thing to remember:

It’s very important that you know your employment status because employees and self-employed people pay tax differently. If someone has been wrongly classed as self-employed when they’re actually employed, that person and the business that hired them could face a bill for unpaid tax, interest on the unpaid tax, and even fines.

Helpful tip:

You can use our free online tool called Check Employment Status for Tax on GOV.UK to work out whether a specific job would count as you being self-employed or not.

Doing a tax return if you’re self-employed

If you’re self-employed, it’s important to keep copies of all your invoices, contracts, and anything you’ve spent on running your business (your expenses).

If you work as a subcontractor, you also need to make a record of any Construction Industry Scheme payment and deduction statements. Your contractor will give you these – they’ll show how much money they’ve taken when they pay you.

You’ll need all of this for your tax return. Our Self Assessment if you’re self employed page can provide further information.

Once you’ve sent us your tax return and everything has been worked out, we may find that you’ve paid more tax through the Construction Industry Scheme than you needed to pay. If that’s the case, you’ll be able to get it back as a refund.

Getting help and support

If you’re still unsure about the Construction Industry Scheme, reverse charge VAT, or your employment status, it can be a good idea to talk to an accountant who knows the construction industry. Getting these things right from the start will help you feel more tax confident so you can avoid any surprises later.